This report explores the major regulatory shifts and institutional developments shaping the tokenized real-world assets (RWA) market in the new U.S. political era following Donald Trump’s inauguration in 2025.

It provides a clear breakdown of evolving crypto regulations, highlights booming institutional adoption of tokenized private credit, real estate, and debt instruments, and showcases Liqvid’s own milestones in this rapidly growing sector.

It provides a clear breakdown of evolving crypto regulations, highlights booming institutional adoption of tokenized private credit, real estate, and debt instruments, and showcases Liqvid’s own milestones in this rapidly growing sector.

Current context:

Since the inauguration of Donald Trump on January 20, 2025, a cautious yet assertive recognition of cryptocurrencies has taken shape at the highest levels of the U.S. government. This has ushered in a fundamentally new regulatory paradigm, marked by active steps toward integrating digital assets into the legal and financial core of the American economy.

At this stage, the direction of U.S. crypto regulation can be divided into three major tracks:

- Bitcoin Regulation

- Stablecoin Regulation

- Altcoin (and RWA) Regulation

This taxonomy reflects the country’s current regulatory priorities, driven by two key legislative and executive developments:

- Creation of the Bitcoin Reserve – signaling Bitcoin's recognition as a strategic digital commodity;

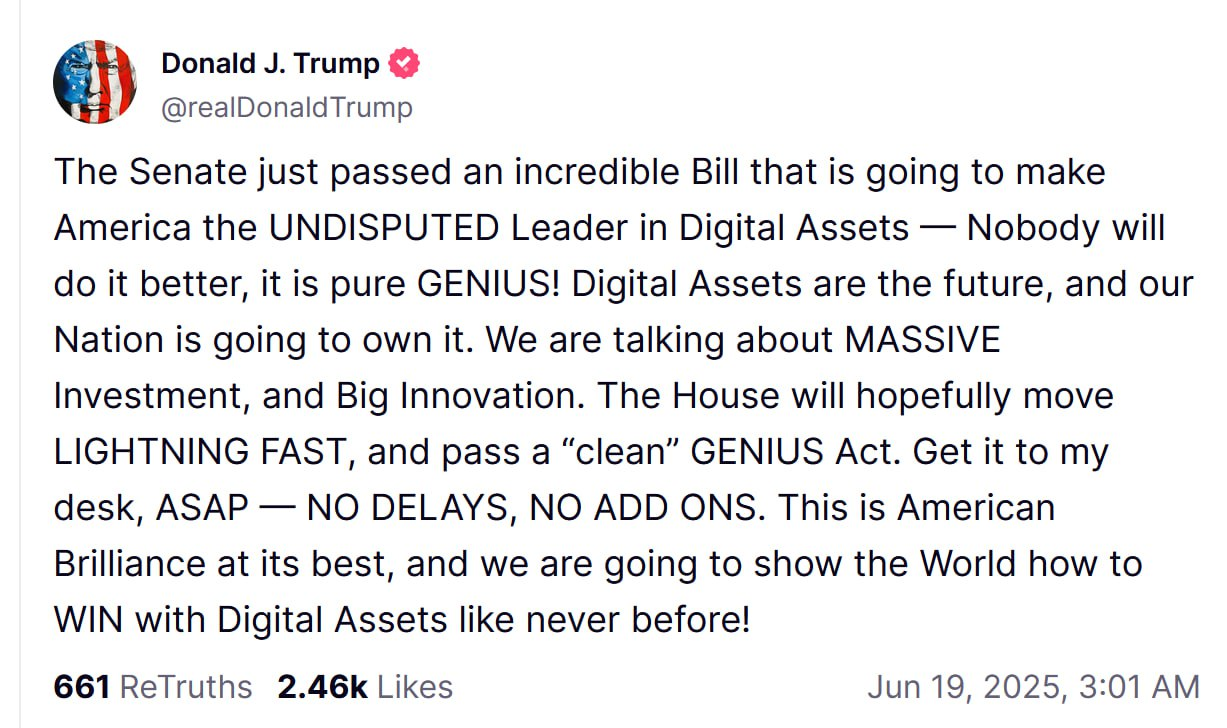

- The GENIUS Act – a landmark bipartisan bill establishing clear requirements for fiat-backed stablecoins, including full collateralization, routine audits, and AML compliance.

In contrast, altcoins remain largely outside the scope of serious regulatory attention. This regulatory asymmetry has manifested in market behavior: Bitcoin and stablecoins are significantly outpacing altcoins in capitalization growth.

Bitcoin Dominance Growth in H1 2025

Yet an important sector - Real World Assets (RWAs) is at the intersection of stablecoins and altcoins also show significant growth in the H1 2025.

RWAs, like stablecoins, are tokenized claims on real-world assets, but unlike altcoins, they are not purely speculative instruments. Instead, they serve as bridges between traditional capital markets and blockchain infrastructure. Given the growing relevance of this category, RWAs are likely to become a key focus of the next regulatory wave.

Indeed, the GENIUS Act, while targeting stablecoins, could easily be adapted to RWA frameworks especially for U.S. Treasuries, real estate, and tokenized debt. If the objective is to bolster macroeconomic indicators such as U.S. capital inflows, stock market capitalization, and foreign demand for Treasuries, then enabling RWA tokenization aligns perfectly with national interests.

Indeed, the GENIUS Act, while targeting stablecoins, could easily be adapted to RWA frameworks especially for U.S. Treasuries, real estate, and tokenized debt. If the objective is to bolster macroeconomic indicators such as U.S. capital inflows, stock market capitalization, and foreign demand for Treasuries, then enabling RWA tokenization aligns perfectly with national interests.

The Trump administration has already laid foundational steps in this direction. In January, it issued the “Strengthening American Leadership in Digital Financial Technology” executive order, which established a Digital Asset Markets Working Group and banned CBDC development, effectively encouraging private innovation in tokenized finance.

The regulatory pivot accelerated with the appointment of Paul Atkins as SEC Chair, a well-known deregulatory figure who swiftly rolled back 14 proposed rules relating to AI, cybersecurity, and digital assets. His approach has significantly reduced friction for crypto-native firms, paving the way for more institutional engagement in RWAs.

For Liqvid, the evolving regulatory landscape opens up new opportunities, as more projects are exploring the tokenization of assets, credit, and financial instruments. At the same time, growing investor confidence is driving increased liquidity into crypto, signaling a shift in attitudes toward on-chain investments.

The regulatory pivot accelerated with the appointment of Paul Atkins as SEC Chair, a well-known deregulatory figure who swiftly rolled back 14 proposed rules relating to AI, cybersecurity, and digital assets. His approach has significantly reduced friction for crypto-native firms, paving the way for more institutional engagement in RWAs.

For Liqvid, the evolving regulatory landscape opens up new opportunities, as more projects are exploring the tokenization of assets, credit, and financial instruments. At the same time, growing investor confidence is driving increased liquidity into crypto, signaling a shift in attitudes toward on-chain investments.

Institutional Momentum

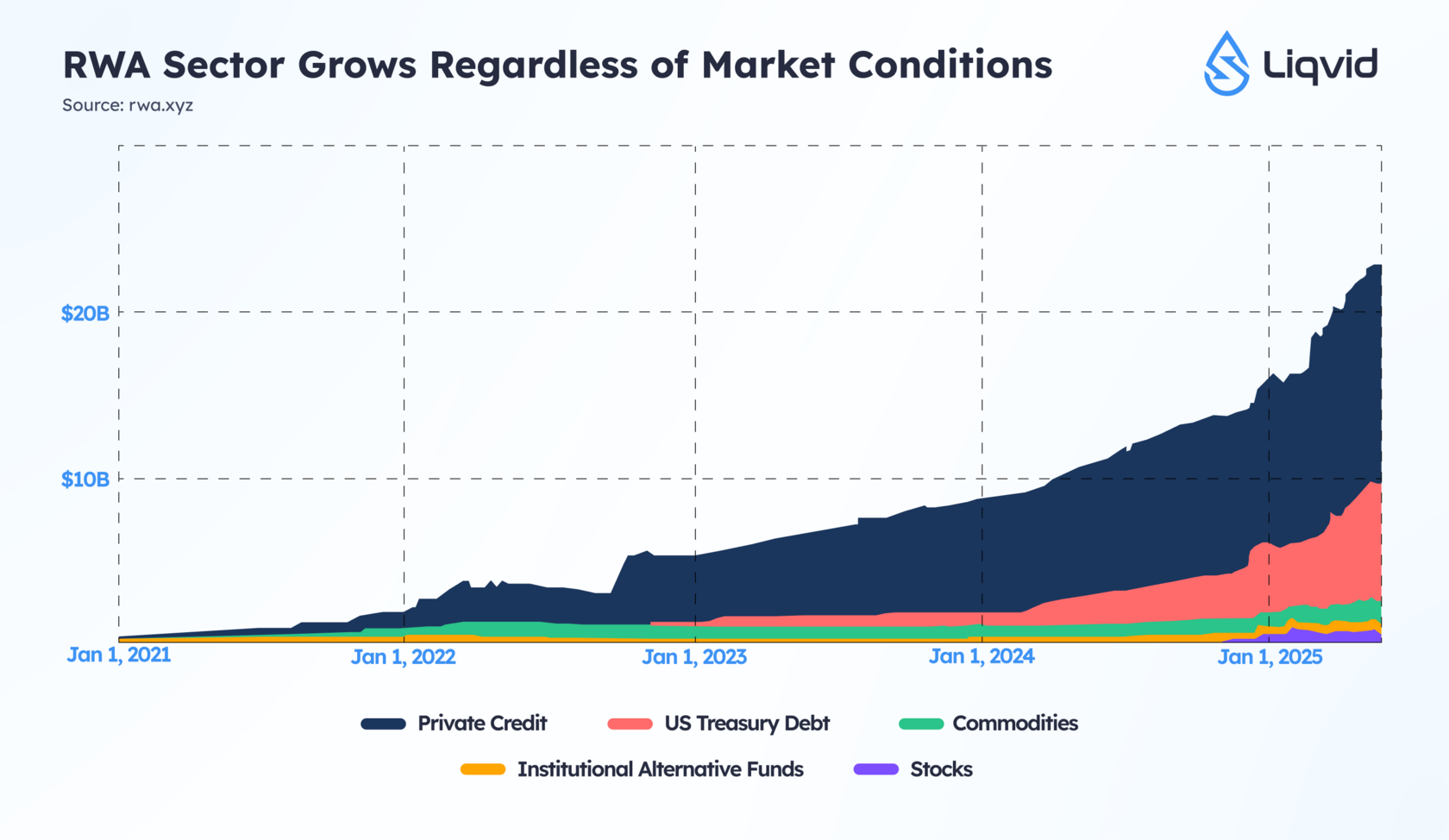

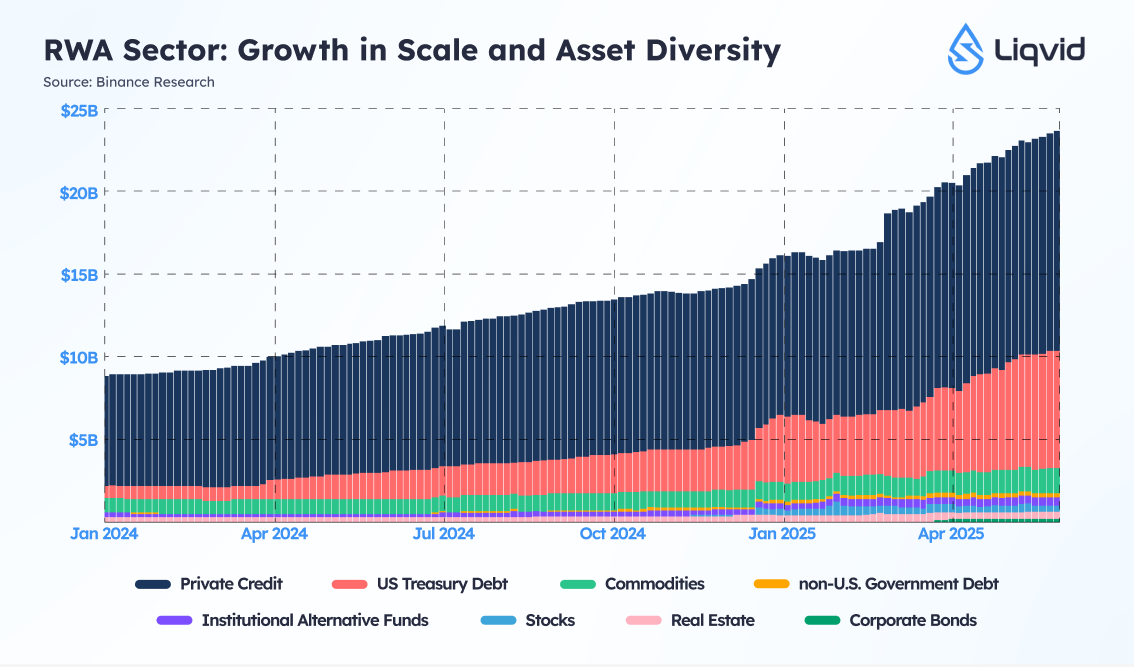

The first half of 2025 has firmly established real-world assets as one of the most rapidly institutionalizing verticals in crypto. No longer confined to proof-of-concept pilots or internal sandbox tests, traditional finance players are now bringing live tokenized products to market at scale. The tokenized RWA market grew from approximately $15.2 billion at the close of 2024 to over $24 billion by mid-2025, marking an 85% year-over-year increase and a 260% surge in issuance volume just in H1 alone. These are not speculative tokens, they represent U.S. Treasuries, private credit, gold, real estate, and money-market funds made natively composable on-chain.

At the heart of this momentum is the convergence of three drivers: a yield-hungry macro environment, advancing regulatory clarity in the U.S., and a maturing infrastructure stack supported by both crypto-native builders and Wall Street incumbents.

Institutional Players Goes From R&D to Market Expansion

Institutions that once treated tokenization as an R&D experiment have now entered production mode. BlackRock, which made headlines with its “BUIDL” tokenized fund in 2024, has since expanded its scope and filed for live issuance in H1 2025.

In parallel, J.P. Morgan launched JPMD, an on-chain deposit token built on Base. The initiative enables fully compliant, programmable transfers of insured deposits, effectively marrying traditional banking safeguards with the speed and flexibility of blockchain rails. This also marks a strategic signal from J.P. Morgan: that Ethereum-compatible networks are seen as viable infrastructure for institutional-grade finance.

On the asset management front, firms like Franklin Templeton is now issuing tokenized fixed-income products and exploring private credit opportunities distributed through DeFi protocols.

On the asset management front, firms like Franklin Templeton is now issuing tokenized fixed-income products and exploring private credit opportunities distributed through DeFi protocols.

Fidelity and VanEck announced they are preparing to launch tokenized fund products in the second half of 2025, pushing traditional asset managers from the sidelines to the main stage.

Infrastructure Start-ups Gain Institutional Backing

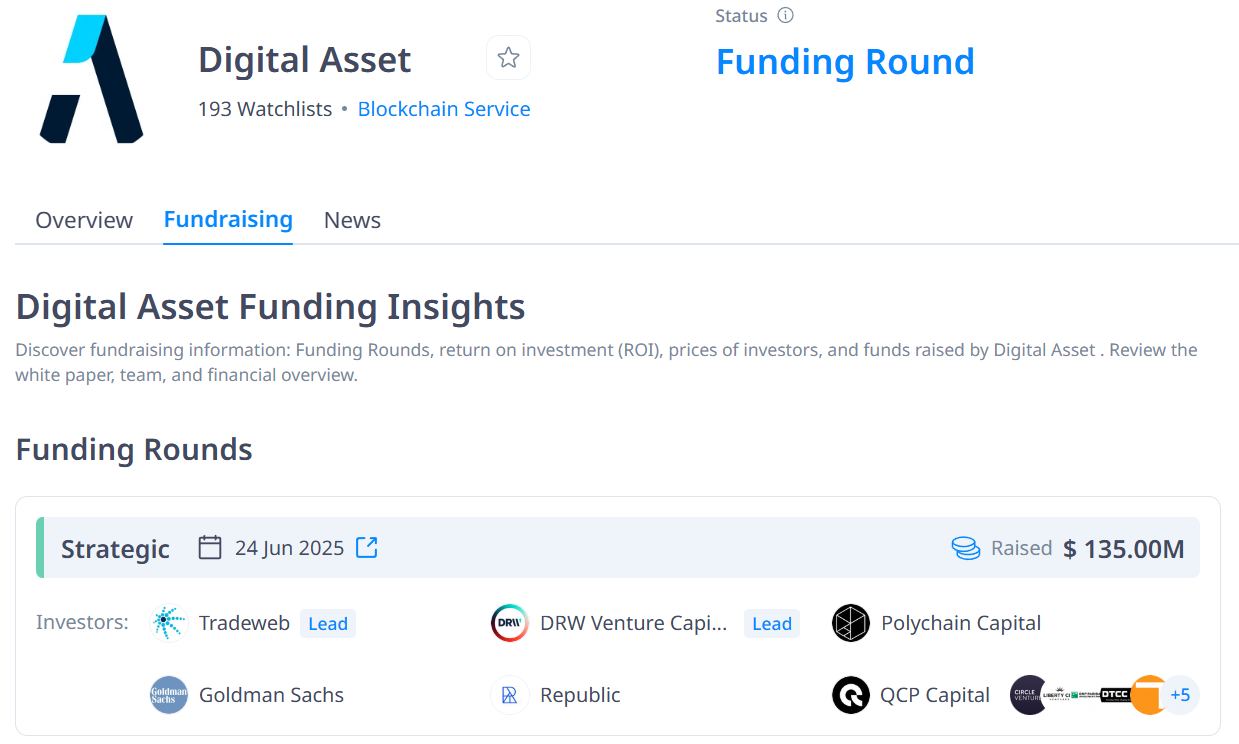

The wave of institutional activity is being matched by growing investment in tokenization infrastructure. In June 2025, Digital Asset raised $135 million in a Series D round led by Goldman Sachs, Citadel Securities, BNP Paribas, and Tradeweb, with support from Microsoft and Deloitte. Their open-source Canton Network, built to enable the privacy and interoperability required by regulated financial institutions, is now used by over 30 major institutions to tokenize eurobonds, commodities, money-market funds, and even tokenized gold. Canton’s development exemplifies the demand for compliant, cross-chain financial systems that allow traditional assets to flow with on-chain efficiency.

Another key player, Securitize, has further entrenched its leadership position in the RWA space. As of June 2025, the firm manages over $2.8 billion in tokenized U.S. Treasuries, representing more than 70% of the tokenized treasuries market. Eight of the top ten RWA tokens by volume are issued through Securitize, and the platform has become the default tokenization layer for a growing number of asset managers and fintechs.

Market Insights & Key Trends

Private credit has emerged as the leading category, accounting for over 58% of total RWA value. Institutional investors are increasingly drawn to this segment by the promise of consistent on-chain yields between 8% and 12%.

Meanwhile, tokenized U.S. Treasuries have rapidly gained adoption, now making up around 34% of the total RWA market. Products from Ondo Finance, Franklin Templeton, and Backed Finance are being integrated into both DeFi and TradFi strategies, serving as low-risk, yield-bearing instruments.

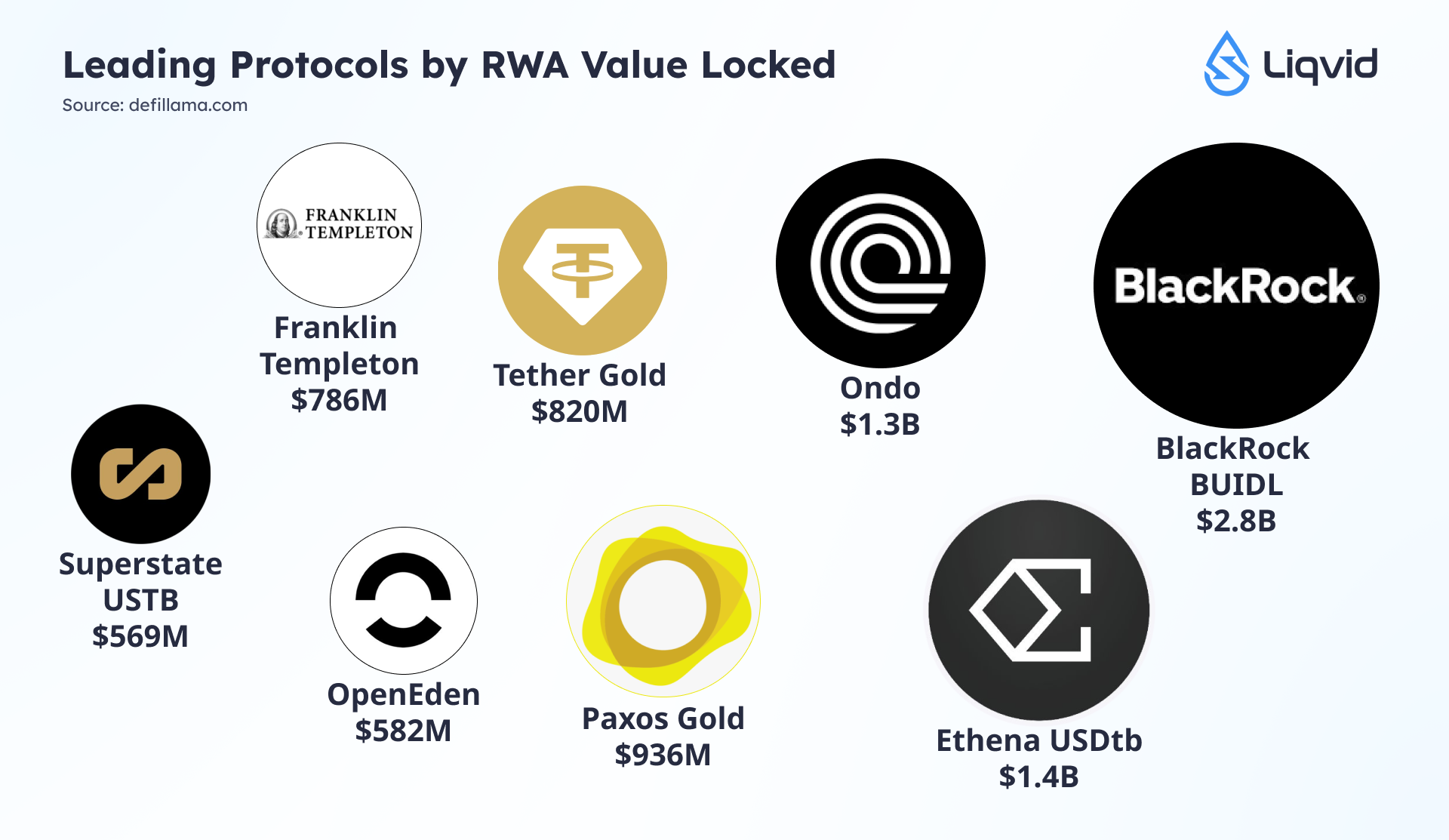

Gold-backed tokens such as Paxos Gold (PAXG) and Tether Gold (XAUT) have also gained traction, each surpassing $800 million in capitalization and reinforcing demand for asset-backed digital assets.

Gold-backed tokens such as Paxos Gold (PAXG) and Tether Gold (XAUT) have also gained traction, each surpassing $800 million in capitalization and reinforcing demand for asset-backed digital assets.

Among the protocols leading this growth, BlackRock’s BUIDL fund has emerged as the dominant force, with total value locked (TVL) reaching $2.8 billion outpacing any other player in the space. It is followed by Ethena’s USDtb, a synthetic dollar product with a TVL of $1.4 billion, and Ondo’s tokenized treasury offering, which has climbed to $1.3 billion.

On the infrastructure side, oracle providers like Chainlink, RedStone, and Pyth Network have played a crucial role in enabling real-time pricing, NAV reporting, and composability for tokenized assets. At the same time, enterprise-grade blockchains are gaining momentum.

Ethereum continues to dominate as the settlement layer of choice, hosting 59% of all RWA value $7.7 billion followed by its layer-2 zkSync with $2.3 billion. However, alternative chains such as Solana, Aptos, Stella, Polygon, Algorand, and Arbitrum are beginning to capture significant share as well, each crossing $300 million in RWA related TVL due to their high throughput and low transaction costs.

Ethereum continues to dominate as the settlement layer of choice, hosting 59% of all RWA value $7.7 billion followed by its layer-2 zkSync with $2.3 billion. However, alternative chains such as Solana, Aptos, Stella, Polygon, Algorand, and Arbitrum are beginning to capture significant share as well, each crossing $300 million in RWA related TVL due to their high throughput and low transaction costs.